Author: Mykhailenko A.

As a provider of cloud infrastructure and data center services, we at Colobridge analyze the technological trends that shape the future of business. In this article, we’ll explore what RegTech is, how these technologies evolved from FinTech, and why they have become indispensable for modern financial organizations.

- The RegTech Market in Numbers

- Key Takeaways

- What is RegTech and Why is Everyone Talking About It?

- How Does RegTech Work? Key Application Areas

- What’s the Difference Between FinTech and RegTech?

- RegTech: A Visual Summary

- Frequently Asked Questions (FAQ)

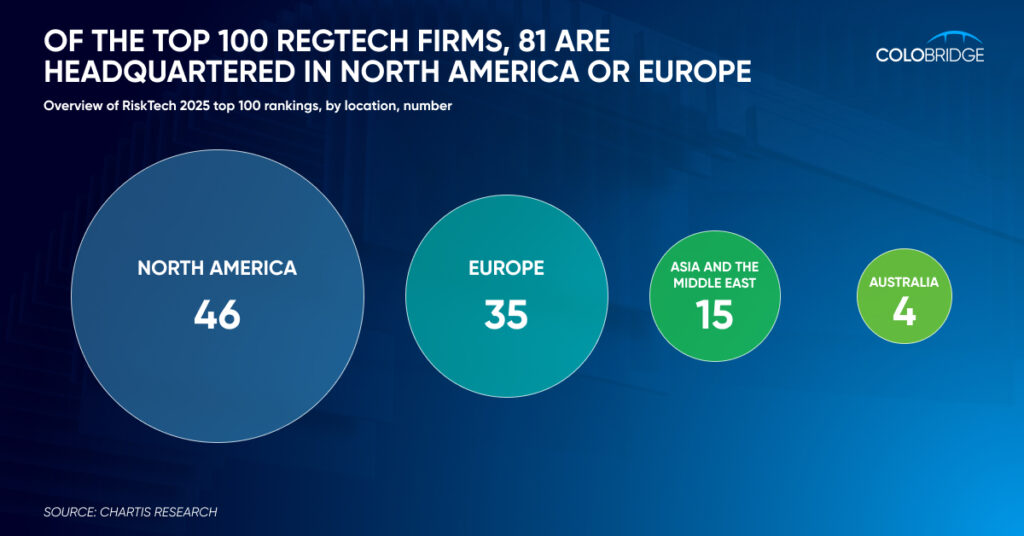

The RegTech Market in Numbers

To understand the scale of regulatory technology’s impact, one only needs to look at the numbers. According to Fortune Business Insights, the global RegTech market was valued at $15.80 billion in 2024 and is projected to reach $82.77 billion by 2032. This explosive growth underscores the critical importance of automation in the compliance sphere.

Key Takeaways

- Defining RegTech: RegTech (Regulatory Technology) is the use of technology, primarily IT, to efficiently and cost-effectively comply with regulatory requirements.

- A Catalyst for Growth: The 2008 global financial crisis led to a sharp increase in the complexity and volume of regulations, making manual compliance management extremely expensive and inefficient.

- Core Functions: RegTech solutions help automate regulatory reporting, transaction monitoring (AML), customer verification (KYC), and risk management.

- Technological Foundation: The backbone of RegTech software consists of cloud computing, Big Data, Artificial Intelligence (AI), and Machine Learning (ML).

What is RegTech and Why is Everyone Talking About It?

RegTech is a sub-sector of FinTech focused on applying technology to solve challenges in regulation and compliance. Simply put, it’s a category of IT solutions that help companies, primarily banks and financial institutions, adhere to an ever-growing number of legal requirements.

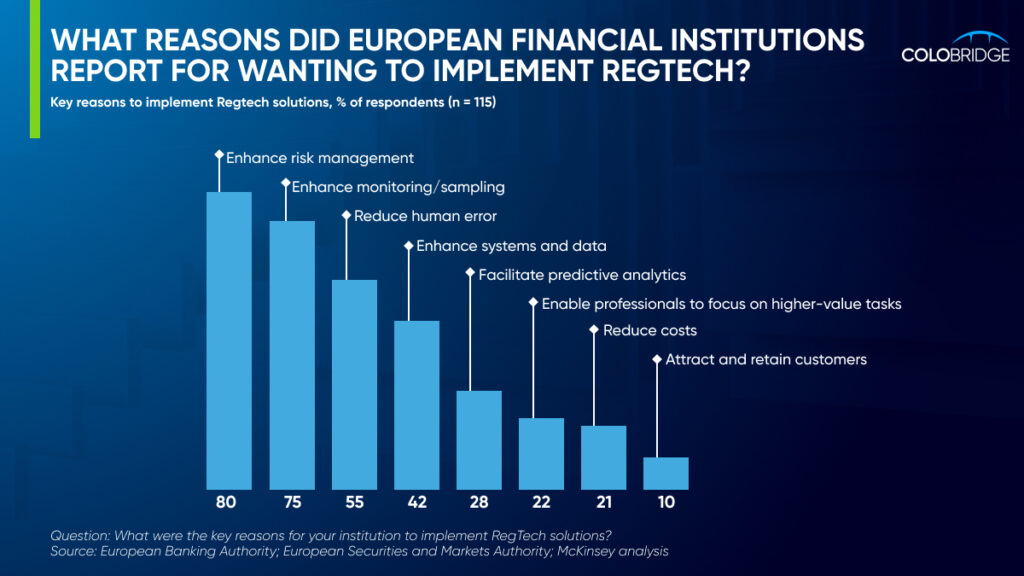

The impetus for the rapid development of the RegTech market was the 2008 financial crisis. In its aftermath, regulators worldwide introduced thousands of new rules to increase the transparency and stability of the financial system. As a result, compliance costs for banks skyrocketed, reaching 10-15% of their operating expenses. It became clear that managing this process effectively without automation and smart technology was impossible.

How Does RegTech Work? Key Application Areas

RegTech software automates and optimizes routine processes, making them faster, more accurate, and cheaper. Here are a few key areas of application:

- Regulatory Reporting: Automatically collecting data and generating reports for supervisory bodies in the required formats.

- Risk Management: Real-time data monitoring and analysis to identify potential risks and fraud.

- Identity Verification: Solutions for KYC (Know Your Customer) and AML (Anti-Money Laundering) that automate customer screening and monitor transactions for suspicious activity.

- Legislative Monitoring: Tracking changes in regulations and automatically updating the company’s internal procedures.

What’s the Difference Between FinTech and RegTech?

Although the terms are closely related, there is a key distinction between them.

- FinTech (Financial Technology) is a broad term covering any technology that improves or transforms financial services. This includes mobile banking, online payments, P2P lending, and much more.

- RegTech is a narrower specialization within FinTech, aimed exclusively at automating regulatory compliance.

Therefore, one could say that all RegTech is a part of FinTech, but not all FinTech is RegTech.

Colobridge Expert:

“From an IT infrastructure perspective, RegTech solutions are a classic example of high-load systems that demand maximum reliability and security. They handle sensitive data, require immense computational power for real-time analysis, and must be available 24/7. This is precisely why cloud platforms have become the de facto standard for deploying such systems. The cloud provides the necessary flexibility for scaling, a high level of data protection, and cost-effectiveness, which is critically important for optimizing compliance costs.”

RegTech: A Visual Summary

| Aspect of RegTech | Key Details from the Article |

|---|---|

| Definition | The use of technology, primarily IT, to efficiently and cost-effectively comply with regulatory requirements. It is a sub-sector of FinTech. |

| Market Growth | The global market was valued at $15.80 billion in 2024 and is projected to reach $82.77 billion by 2032. |

| Primary Driver | The 2008 global financial crisis, which led to a sharp increase in the complexity and volume of regulations. This made manual compliance extremely expensive and inefficient. |

| Core Applications | – Automating regulatory reporting – Managing risk through real-time data monitoring and analysis – Verifying customer identity (KYC) and monitoring for money laundering (AML) – Tracking changes in legislation and updating internal procedures |

| Key Technologies | – Cloud Computing – Big Data – Artificial Intelligence (AI) and Machine Learning (ML) – Blockchain for creating reliable identity systems and tracking transactions |

| Key Benefits | – Reduced compliance costs – Increased accuracy and speed of reporting – Minimization of human error – The ability to adapt quickly to new regulatory requirements |

| Primary Users | – Primarily banks, insurance companies, and investment funds – Solutions are increasingly accessible to small and medium-sized enterprises (SMEs) thanks to the cloud and SaaS models |

| Future Outlook | The future lies in using predictive analytics and AI to shift from reactive compliance to proactive risk management. There will also be a move towards more integrated, seamless “platform” approaches. |

Frequently Asked Questions (FAQ)

1. What is RegTech in simple terms?

RegTech is the use of modern technology (like AI and cloud computing) to help companies, especially banks, comply with complex financial laws and regulations automatically and at a lower cost.

2. What are the main benefits of RegTech?

The primary advantages are reduced compliance costs, increased accuracy and speed of reporting, minimization of human error, and the ability to adapt quickly to new regulatory requirements.

3. What kinds of companies use RegTech solutions?

Primarily banks, insurance companies, investment funds, and any other financial sector organizations. However, as regulation in other industries becomes more complex (e.g., GDPR in IT), RegTech is finding applications beyond the financial sector.

4. Is RegTech a part of Artificial Intelligence?

Not exactly. RegTech is an application area, while Artificial Intelligence (AI) is one of the key technologies used within RegTech solutions to analyze data, detect anomalies, and predict risks.

5. What are the main challenges of implementing RegTech?

The main difficulties include integrating new solutions with existing legacy IT systems, the high initial cost of implementation, ensuring data privacy and security, and a shortage of skilled professionals who understand both technology and regulatory requirements.

6. What role does blockchain play in RegTech?

Blockchain offers unique opportunities for RegTech due to its immutability and transparency. It can be used to create reliable identity systems (KYC), track transactions (AML), and automate the execution of smart contracts, which significantly increases trust and reduces the risk of fraud.

7. How does RegTech handle privacy rules like GDPR?

RegTech solutions help automate compliance with data protection rules. They can manage user consent, track the processing of personal data, automatically apply anonymization policies, and generate reports to prove compliance with GDPR or other similar laws.

8. Will RegTech replace compliance officers?

No, RegTech will not replace people but rather augment their capabilities. Technology will take over routine, repetitive tasks like data collection and monitoring, allowing compliance officers to focus on strategic analysis, complex decision-making, and interaction with regulators.

9. Can small and medium-sized enterprises (SMEs) use RegTech?

Yes. Although RegTech was initially geared towards large banks, the rise of cloud computing and the SaaS (Software as a Service) model is making these solutions increasingly accessible to SMEs. This allows them to automate compliance and compete with larger players without massive capital investment.

10. What is the future of RegTech?

The future of RegTech lies in greater use of predictive analytics and AI to move from reactive compliance (reporting on past events) to proactive risk management (preventing issues before they occur). We will also see increased integration and a “platform” approach, where various RegTech tools work together seamlessly.